Blog

“A History of the Federal Funds Rate“

There is a lot of talk about the Federal Funds rate recently and whether or not the Federal Reserve will lower interest rates in 2024. I thought this recent article from Yahoo Finance did a good job explaining the history of where the fed funds rate has been and reasons for why it might change in the near future.

Enjoy Reading!

You may not think much about the federal funds rate day to day, but this key number impacts many areas of your financial life and the economy as a whole.

The Federal Reserve — the country’s central bank — periodically adjusts its target rate to keep the economy running smoothly and consumer prices in check. When the federal funds rate moves up or down, so do the interest rates on bank accounts and loans. In other words, changes in the Fed’s rate impact how much your savings can grow and how much you pay to borrow money.

What is the federal funds rate?

The federal funds rate is set by the Federal Reserve and dictates what a bank can charge another bank for ultra-short-term loans (usually overnight) in order to meet reserve requirements. It’s expressed as a range, and financial institutions can negotiate a specific rate between each other within that range.

The Fed’s target rate also impacts the interest rates individual financial institutions set for financial products such as deposit accounts, bonds, loans, and credit cards.

Currently, the Fed’s target range stands at 5.25%-5.50%; the Fed is expected to continue holding its target rate steady until inflation cools further.

Historical Fed interest rate: How it’s changed over 50 years

Though the Fed has not adjusted the federal funds rate since July 2023, this rate has fluctuated quite a bit in the past few decades in response to major economic and world events.

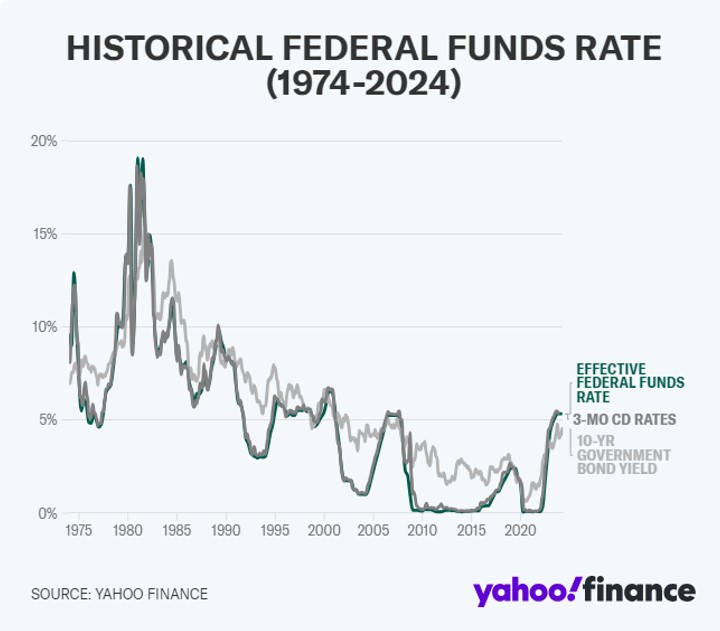

Here’s a look at the effective federal funds rate since 1974, along with 3-month CD rates and 10-year government bond yields, so you can see how the Fed’s rate impacts other interest rates.

The federal funds rate soared in the early 1980s when inflation hit more than 13%, the highest level recorded. This marked the end of a macroeconomic period known as the “Great Inflation,” which economists believe was brought on by Federal Reserve policies that led to an overgrowth in the supply of money.

In response, the Fed raised interest rates, and the federal funds rate reached more than 19%.

In the late 1990s and into the early 2000s, there was another major economic shift when the Fed began bringing the federal funds rate down. This move was fueled by the dot-com bubble burst — a period of economic instability when investors poured capital into internet-based companies, which led to an overvaluation of many of these start-ups. Unfortunately, not all of these companies were profitable, and the fallout of this bubble burst led to many bankruptcies and a recession.

Then, following the terrorist attacks of Sept. 11, 2001, the Fed cut rates further due to widespread uncertainty and a slowdown in economic activity.

In 2007, the housing market crash prompted the Fed to once again lower its target rate to 2%. A series of rate cuts followed, eventually bringing the target range down to a range of 0%-0.25% — effectively zero — by December 2008.

As the economy recovered from the Great Recession, the Fed began slowly increasing rates again. But in 2020, the COVID-19 pandemic rocked the U.S. economy and brought about challenges such as supply-chain issues, reduced economic activity, and high unemployment. In March 2020, the Fed once again slashed rates to a range of 0%-0.25%.

Since then, the Fed has increased its rate by 0.25 basis point increments to combat skyrocketing inflation. Today, the inflation rate still hasn’t reached the Fed’s desired 2% target, so it has held rates steady.

What to expect from the Fed moving forward

The Fed’s next meeting is slated for the middle of September when the Federal Open Market Committee (FOMC) will decide whether or not to adjust the federal funds rate. In its last meeting (June 12th), the Fed announced that it would maintain its target range at 5.25%-5.50% and continue to monitor the economic situation before considering cuts.

The Fed reiterated in a statement last month that it would adjust this rate as it sees fit, but rates will probably hold steady for the time being:

“In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2%.”

Ultimately, the Fed’s primary responsibility is to maintain a stable economy through the monetary policies it enacts and promote economic growth. Over time, it has adjusted its stance based on the current economic conditions. What holds true is that these changes to the federal funds rate, no matter how small, impact everyday consumers and can influence their financial decisions.